The geography, political economy and international geopolitics of fertilisers

On the weekend of February 28-March 1, hours after shipping in the Strait of Hormuz shut down following US military strikes on Iran, global fertiliser prices began to rise. The reaction was swift and instructive. It was a vivid demonstration of the food system’s structural vulnerability and dependence on supply chains that are geographically concentrated and acutely sensitive to geopolitical shocks.

Every loaf of bread, bowl of rice, and plate of vegetables on our table owes something to fertilisers, the unglamorous but vital chemical backbone of modern agriculture. Without them, the food system as we know it wouldn’t function. Understanding where fertiliser sources come from, which companies make them, and how their production is structured is increasingly a matter of national interest. A quarter of the United Kingdom’s manmade fertiliser is used for cereals production, about half of which goes for human use, while half is applied to grass to make it grow more abundantly for meat and dairy production. The country produced 371 000 tonnes of fertiliser in 2019-21, but imported 1 287 000 tonnes in the same period, meaning it would be particularly exposed to any shortage. It is not alone.

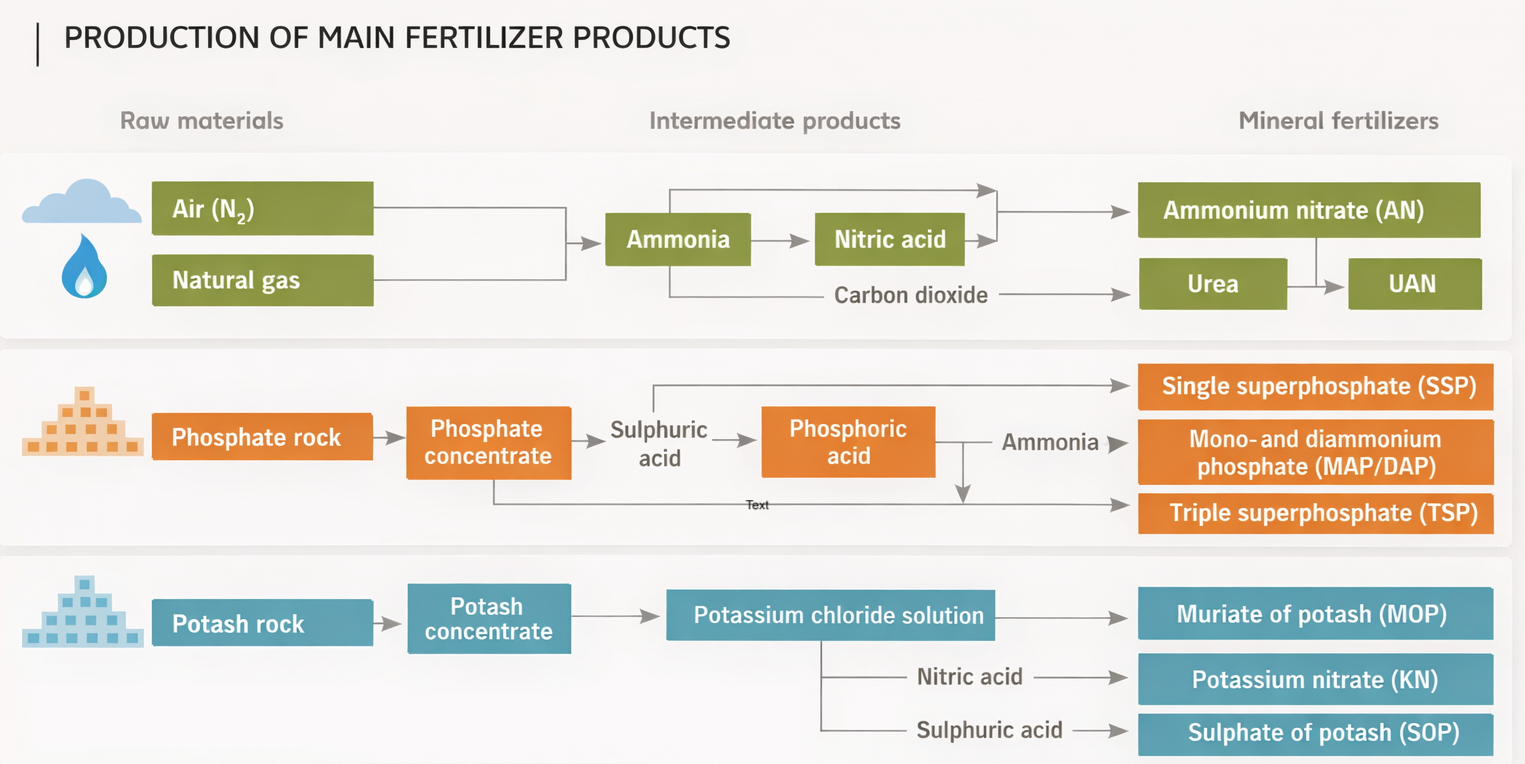

The three pillars of N, P and K

Soils used in agriculture become depleted in the nutrients necessary for plant growth and must be regularly replenished. The three most important macronutrients are nitrogen, phosphorus, and potassium, each carrying its own set of supply chain vulnerabilities.

Figure reproduced from Fertilizers Europe

Nitrogen (N) is the most important macronutrient for plant growth and development and for high yields. The Haber-Bosch process -one of the most significant chemical innovations of the 20th century- converts atmospheric nitrogen (N₂) into ammonia using fossil fuels such as natural gas or coal as a hydrogen source. Nitrogen fertiliser should therefore be considered predominantly as an energy product: when gas prices spike (as they did across Europe in 2022 following the Russian invasion of Ukraine) nitrogen fertiliser costs follow, often sharply.

Phosphorus(P) is vital for root development and drought resistance, while potassium(K) helps improve crop quality. Unlike nitrogen, phosphorus and potassium cannot be synthesised from the air: both require raw materials (phosphate rock and potash rock) to be mined, before being treated, concentrated and converted into forms that can be directly absorbed by plants. The vast majority -over seventy percent- of phosphate rock reserves are found in Morocco and the Western Sahara. Production is being stepped up in Brazil, Kazakhstan, Mexico, Morocco, and Russia. Most of the world’s reserves of recoverable potash ore are concentrated in Canada and in Belarus. The food system is built on natural inputs that are geographically fixed and relatively finite. That tension is not going away.

A world map of concentration

The geographical distribution of fertiliser production is striking in its unevenness. In a globalised food system that increasingly aspires to be more resilient, this uneven distribution is more than a little alarming.

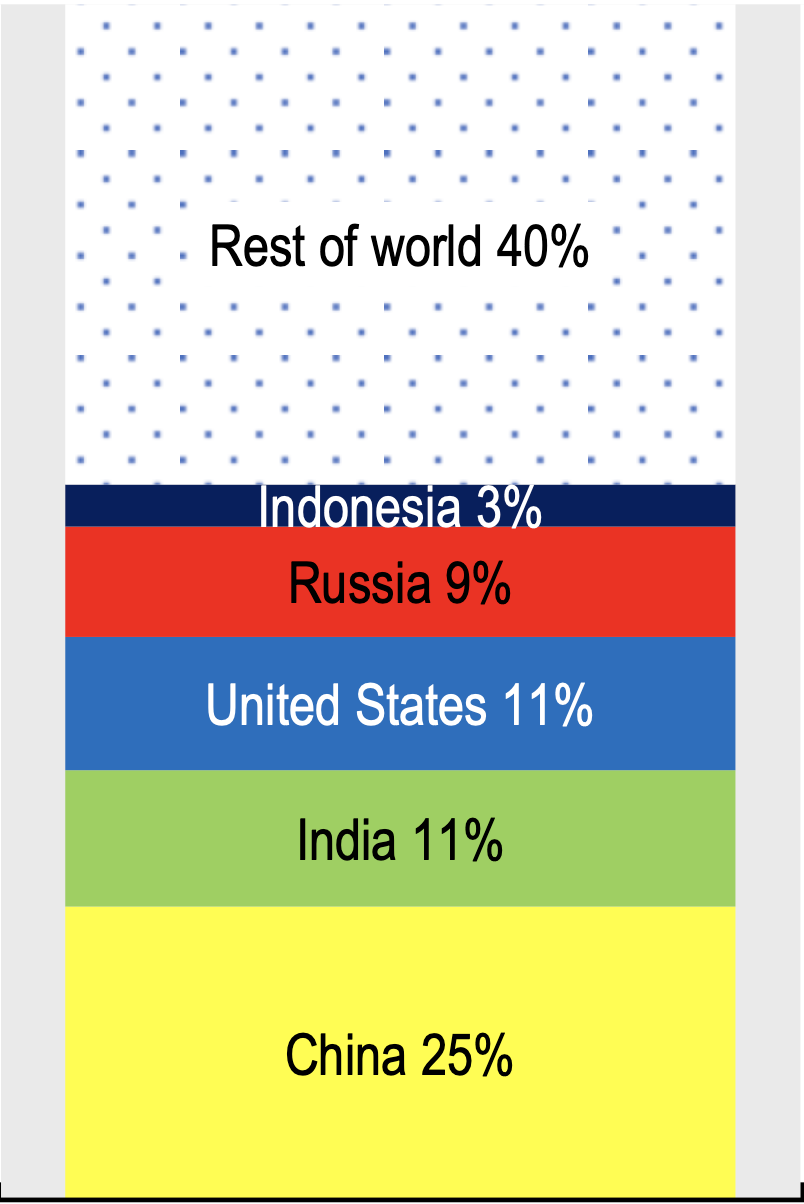

The nitrogen fertiliser sector is the most relatively dispersed of the three. China accounts for roughly a quarter of global production; India and the United States each contribute approximately eleven per cent; Russia provides around nine per cent; and Indonesia around three per cent. The remaining forty per cent is shared among the rest of the world.

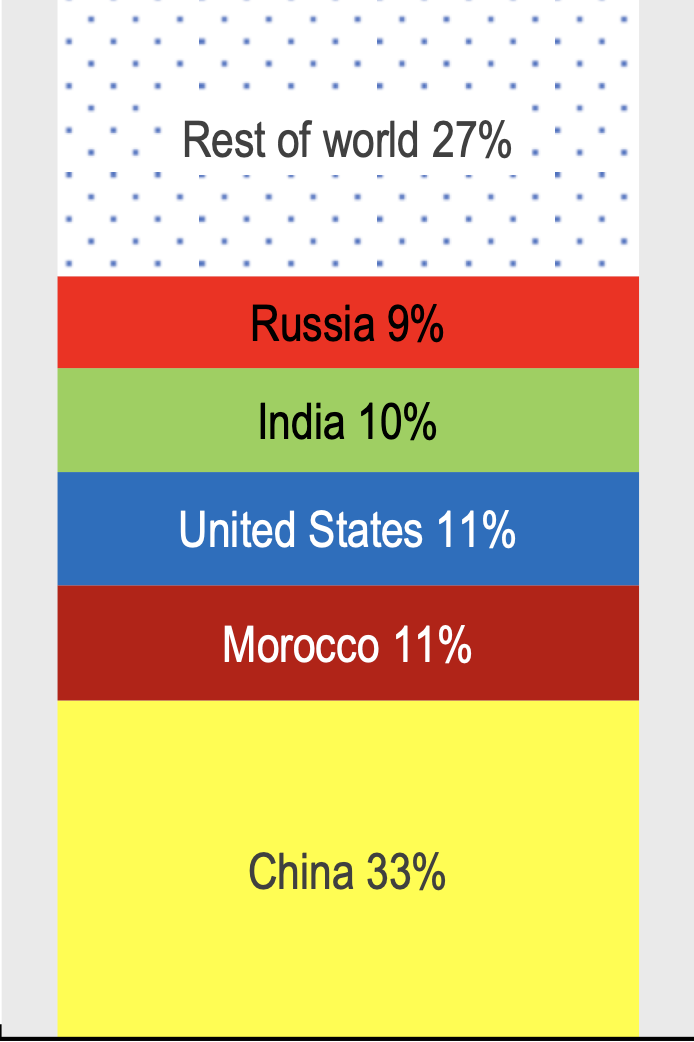

Phosphate fertiliser production is considerably more concentrated. China leads with a third of global output. Morocco, the United States, India, and Russia each account for roughly nine to eleven per cent. Together, these five countries produce nearly three-quarters of the world's phosphate fertilisers: a degree of concentration that ought to invite serious strategic reflection.

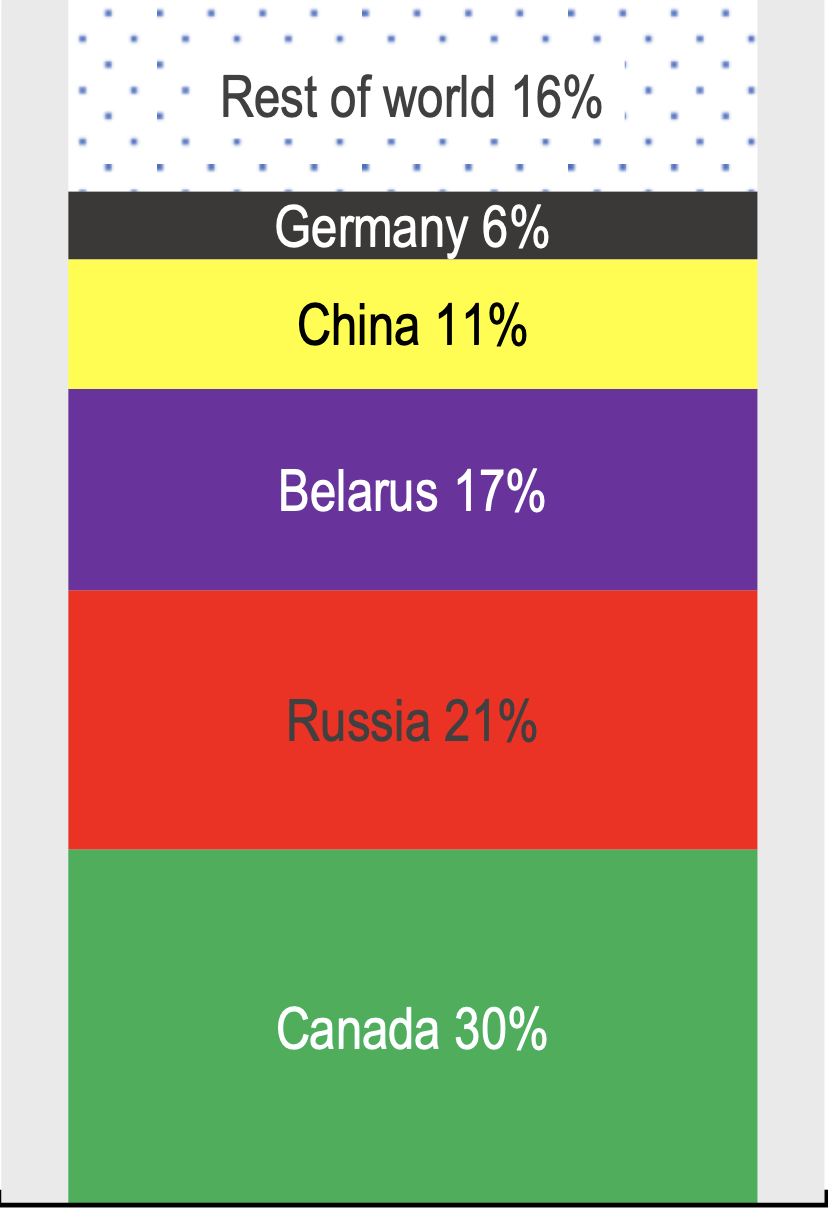

The potash sector is the most concentrated of all. Canada is the dominant potash producer, accounting for thirty per cent of global supply. Russia and Belarus together contribute nearly forty per cent, a fact that became acutely relevant following Russia's invasion of Ukraine in 2022 and the international sanctions that ensued. China accounts for eleven per cent, and Germany for six per cent.

Production statistics reproduced from OECD (2024)

China is increasingly regarded as an emerging 'fertiliser superpower'. While the majority of its production is utilised domestically, China’s dominance across all three nutrient categories, as well as its willingness to impose export controls, should focus the minds of policy makers in importing nations.

There are, however, some welcome signs of diversification. Potash production is expanding in Laos. Phosphate production is increasing in Brazil and the United States. Urea production (urea being the most common solid nitrogen fertiliser) is expanding in Nigeria, Brunei, India, and Brazil. Ammonia production is growing in Iran and in China, and investment in new capacity is emerging in Nigeria, Germany, the Netherlands, and Hungary. In addition, a significant deposit of phosphate rock -estimated at 70 billion tonnes- has recently been identified in southern Norway. While biofertilisers are an alternative, there are still supply and quality issues, and the biofertilsier market remains very small and nascent worldwide. These shifts in production are meaningful and encouraging. The pace, however, remains slower than the risks would warrant.

Corporate concentration

If the geography of fertiliser production is concerning, the industrial structure of the sector compounds those concerns. The fertiliser industry is not merely unevenly distributed across the globe: it is also highly concentrated at the corporate level. This concentration takes different forms across the three nutrient categories, and the ownership structures involved (from publicly listed multinationals to state-controlled enterprises and sovereign wealth vehicles) make the politics correspondingly complex.

The OECD has noted, with some understatement, that corporate concentration of fertiliser production can be attributed to natural resource endowments and economies of scale 'rather like the oil industry'. The parallel is reflected in profit figures: the global think tank has calculated that the combined profits of the world’s nine biggest fertiliser companies quadrupled from 13 billion US dollars in 2020 to 55 billion US dollars just two years later. The beneficiaries of the post-Ukraine invasion energy crisis were precisely the companies with the greatest market power.

Leading nitrogen producers include the US-based CF Industries (the world’s largest manufacturer of nitrogen-based fertilisers), Norway-based Yara International, and the Qatar Fertilizer Company (QAFCO). Phosphate fertiliser producers include OCP Group, based in Morocco, US-based Mosaic (the largest producer of finished phosphate products, formed in 2004 following the merger of IMC Global and Cargill’s crop nutrition division), Russia-based PhosAgro (Europe’s largest producer phosphate-based fertilisers) and the Saudi Arabian Mining Company (Ma’aden), which operates the largest phosphate mining facility in the world. The world’s most important potash producers include Canada-based Nutrien, formed in 2018 following the merger of Agrium and the Potash Corporation of Saskatchewan,ICL Group (formerly Israel Chemicals Ltd), K+S AG (Europe’s largest supplier of potash fertiliser), Belarus-based Belaruskali, and the Chilean mining company Sociedad Química y Minera (SQM).

Ownership structures matter as much as market share. Nutrien, CF Industries, Mosaic, ICL Group, K+S AG, PhosAgro and SQM are all publicly listed. Yara International is also publicly listed, but one-third owned by the Norwegian government. QAFCO is a subsidiary of Industries Qatar, itself a subsidiary of the state-owned enterprise QatarEnergy. The Saudi government owns fifty percent of Ma’aden. OCP Group and Belaruskali are entirely state owned. In a sector where state actors play this prominent a role, the boundaries between corporate strategy and foreign policy are, at best, porous.

Responses from policymakers

Unsurprisingly, these levels of concentration have come under scrutiny by academics and policymakers. As early as 2013, Professor C. Robert Taylor and Dr Diana L. Moss of the American Antitrust Institute raised substantive concerns that the global fertiliser industry exhibited the characteristics of an oligopoly, with evidence of anticompetitive coordination among producers that would require, in their assessment, concerted regulatory action to address. Their analysis highlighted the sector's tendency toward price coordination and the structural barriers to new market entrants.

Over a decade later, there are signs that policymakers have, belatedly, started to pay attention. Concern about concentration in the agricultural inputs sector transcended party lines in the United States in September 2025, when Senators Chuck Grassley (Republican-Iowa), Joni Ernst (Republican-Iowa) and Tammy Baldwin (Democrat-Wisconsin) introduced the bipartisan Fertilizer Research Act, co-sponsored by Senator Raphael Warnock (Democrat-Georgia). The proposed legislation required the US Department of Agriculture to conduct a study on competition and trends in the fertiliser market and their subsequent impacts on price. The Act was endorsed by a broad coalition of farming interests, including the National Corn Growers Association, the American Soybean Association, the American Farm Bureau Federation, the National Farmers Union, the Farm Action Fund, the Iowa Farmers Union, the Iowa Farm Bureau, the Iowa Corn Growers Association (ICGA) and the Iowa Soybean Association.

In a parallel move ten days later -possibly in reaction to the bipartisan request- the Assistant Attorney General of the US Justice Department’s Antitrust Division and the General Counsel of the US Department of Agriculture announced a memorandum of understanding to coordinate efforts to protect competition in key agricultural markets, explicitly including fertilisers. Subsequently, in an address to the National Agricultural Law Center, the United States Deputy Secretary of Agriculture Stephen Vaden went further, describing Nutrien and Mosaic’s grip on the fertiliser market as a ‘duopoly’ constraining supplies and driving up costs for farmers, and accusing the two companies of collusion to limit US fertiliser supply and to control prices.

That lawmakers from both parties, two of the most powerful executive agencies in Washington, leading agricultural business interests, and the second-highest-ranking official in the United States Department of Agriculture should find common cause on the issue of corporate concentration in the fertilisers sector speaks to the degree of concern now circulating within the American agricultural establishment. The bipartisan outrage and diagnoses signal a rare moment of political clarity. The true test will be whether this legislative appetite will last and if it will result in durable structural reform, both in the United States and internationally.

Geopolitical chokepoints

Geographic and corporate concentration converge on a third vulnerability: the infrastructure through which fertilisers must travel before they ever reach a field. That infrastructure runs through a small number of chokepoints, all of which are exposed to disruption by conflict, sanctions, or accident.

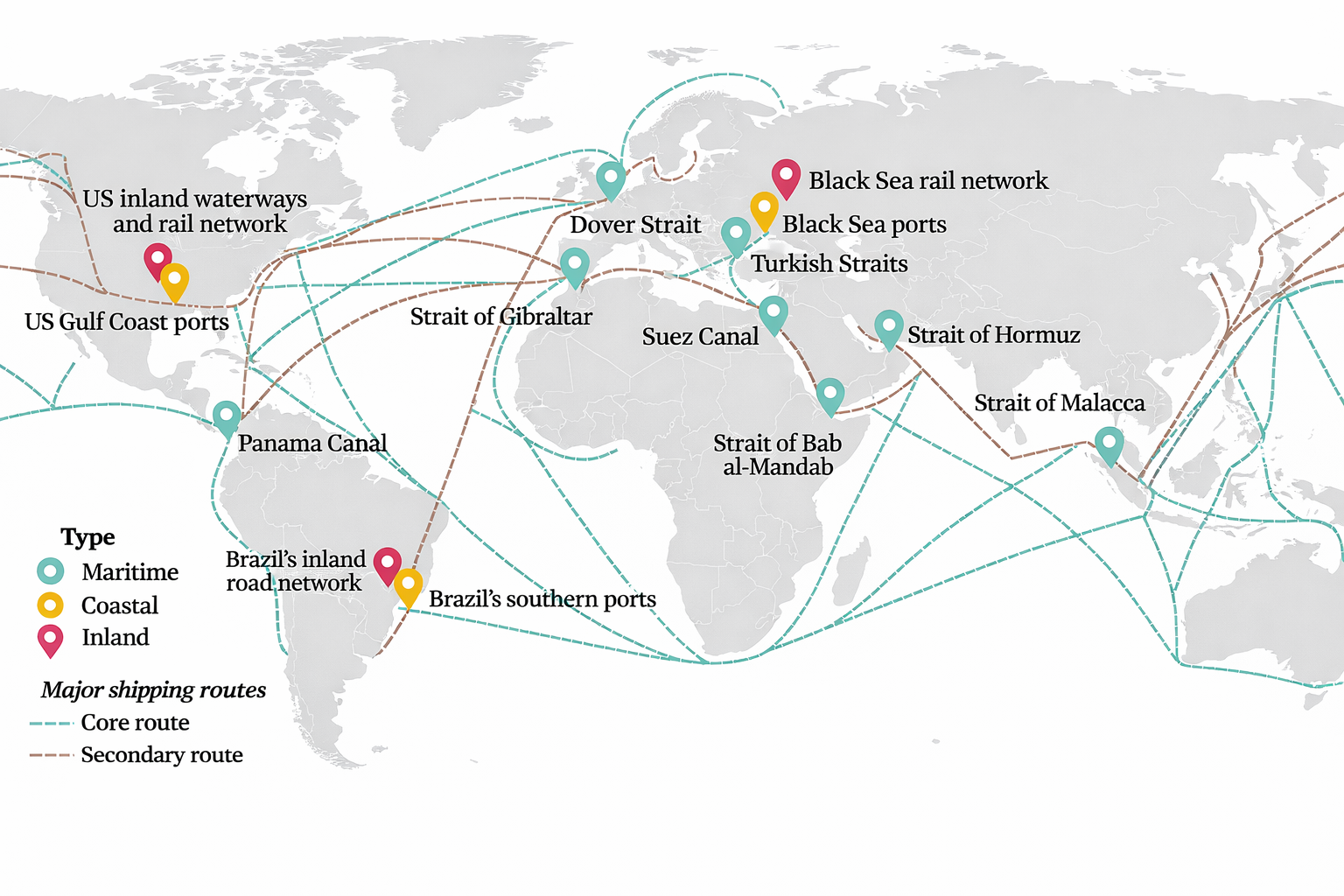

Map reproduced from The Royal Institute of International Affairs (Chatham House)

Shipments of fertilisers, or the raw materials needed to produce them, including natural gas, phosphate rock and potash rock, are particularly vulnerable to disruptions at these chokepoints. Maritime chokepoints, which can be shut down in times of war, are also incredibly narrow. At their narrowest point, the Turkish Straits are just 1 kilometre wide, and the Strait of Malacca just 2.5 kilometres wide.

The Panama and Suez canals, the Strait of Gibraltar and the Strait of Bab al-Mandab are considered of ‘high’ criticality, meaning that the only alternative route is one that would incur a significantly longer transit time and significantly higher shipping costs. The Strait of Hormuz and the Turkish Straits, on the other hand, are considered of ‘very high’ criticality, meaning that no obvious alternative maritime route is available.

The vulnerability of overland infrastructure is equally acute. In one case the risks have already become reality. The 2 470 km long Togliatti-Odesa pipeline was built in 1975-1981 and was capable of exporting 2.5 million tonnes of ammonia to three Black Sea ports in southern and western Ukraine each year. Operation of the pipeline ceased following Russia’s invasion in early 2022. Although Russia and Ukraine had recognised the importance of fertiliser to global food security and struck a deal in June 2022 to allow the safe passage of ammonia through the pipeline despite military hostilities, the pipeline was damaged and rendered inoperable in June 2023. The chokepoints on which our food system depends are not merely vulnerable in theory. Some of them are already broken.

Conclusion

What does all of this add up to? The fertilisers that underpin our food supply are derived from materials extracted in a handful of countries, processed by a handful of corporations, and transported through a handful of narrow straits and pipelines, some of which now pass through active conflict zones.

We have constructed a global food system that is extraordinarily productive and, by the same token, extraordinarily brittle. It functions well until the point at which it does not.

The opening of this article described fertiliser prices rising within hours of shipping disruption in the Strait of Hormuz. That wasn’t a hypothetical scenario: it happened just last weekend. The Togliatti-Odesa ammonia pipeline, which once carried millions of tonnes of fertiliser feedstock annually from Russia to the Black Sea, has been damaged twice since 2022 and is no longer operational. The Strait of Malacca, through which a substantial share of Asia's fertiliser trade must pass, is two and a half kilometres wide at its narrowest point: global fertiliser supplies would come under even further strain if China were to attack Taiwan and lock down a further artery in the global food supply.

The United Kingdom isn’t a bystander to these risks. It produces less than a third of the fertiliser it consumes, has no significant potash reserves, and learned over the last few years as the country’s final ammonia plants closed how quickly the domestic supply chain can reach breaking point. These risks are not abstract: they are features of the physical infrastructure on which our food system depends. Governments, regulators, and the industry itself face choices about how exposed to leave it. We would do well to start making different ones.

This article was published in March 2026. It was subsequently refined with input from Professor Emeritus Tim Lang and featured by the National Preparedness Commission in April 2026.

References

Tim Lang, Natalie Neumann and Antony So, ‘Just in Case: narrowing the UK civil food resilience gap’, main report to the National Preparedness Commission, February 2025.

U.S. Geological Survey, Mineral Commodity Summaries, phosphate rock. February 2026.

U.S. Geological Survey, Mineral Commodity Summaries, potash. February 2026.

Professor Margarita M. Balmaceda, ‘The geopolitics of fertilizer supply chains: implications of the war in Ukraine’, presentation to RIFS Potsdam, October 2023.

International Fertilizer Association, November 2022, February 2025, June 2025.

Tessa Parry-Wingfield, ‘What lies beneath - new phosphate mining industry in Norway’, Institute of Materials, Minerals & Mining, December 2023.

Sanjay Kumar Joshi and Ajay Kumar Gauaha, ‘Global biofertilizer market: Emerging trends and opportunities’, Trends of Applied Microbiology for Sustainable Economy, May 2022.

Organisation for Economic Co-operation and Development, ‘Understanding the resilience of fertiliser markets to shocks: an overview of fertiliser policies’, OECD Food, Agriculture and Fisheries Paper No 208, June 2024.

C. Robert Taylor and Diana L. Moss, ‘The Fertilizer Oligopoly: The Case for Global Antitrust Enforcement’, The American Antitrust Institute, 2013.

Grassley, Baldwin, Ernst Reintroduce Fertilizer Research Act. US Senate, September 16, 2025.

Justice Department and USDA Coordinate to Protect Competition in Agricultural Inputs, September 29, 2025.

Farm Policy News, University of Illinois Urbana-Champaign, ‘USDA’s Vaden Accuses Nutrien, Mosaic of Fertilizer Price Collusion’, January 26, 2026.

Rob Bailey and Laura Wellesley, ‘Chokepoints and Vulnerabilities in Global Food Trade’, The Royal Institute of International Affairs (Chatham House), June 2017.

Reuters, ‘Russia and Ukraine say ammonia pipeline was damaged, in potential blow to grain deal’, June 7, 2023.

BBC News, ‘Ukraine war: Russia says ammonia pipeline blast may end grain deal’, June 8, 2023.